Bihar Board 12th Accountancy Model Papers

Bihar Board 12th Accountancy Model Question Paper 3 in English Medium

Time : 3 Hours 15 Min

Full Marks: 100

Instructions for the candidates

- Candidates are required to give their answers in their own words as far as practicable.

- Figures in the right-hand margin indicate full marks.

- While answering the questions, the candidate should adhere to the word limit as for as practicable.

- 15 minutes of extra time has been allotted for the candidate to read the questions carefully.

- This question paper has two sections: Section – A and Section – B.

- In Section – A, there are 50 objective type questions which are compulsory, each carrying 1 mark. Darken the circle with black/blue ball pen against the correct option on OMR Sheet provided to you. Do not use Whitener/Liquid/Blade/Nail on OMR Sheet, otherwise, the result will be treated as invalid.

- In Section – B there are Non-objective type questions. There are 25 Short answer type questions, out of which any 15 questions are to be answered. Each question carries 2 marks. Apart from this, there are 8 Long answer type questions, out of which any 4 of them are to answer. Each question carries 5 marks.

- Use of any electronic device is prohibited.

Objective Type Questions

Question No. 1 to 50 have four options, out of which only one is correct, you have to mark the correct option on the OMR Sheet. (50 × 1 = 50)

Question 1.

Income & Expenditure Account records transaction of-

(a) Revenue nature only

(b) Capital nature only

(c) Both revenue and capital nature

(d) None of these

Answer:

(a) Revenue nature only

Question 2.

Donations received for special purposes-

(a) Should be credited to income & expenditure A/c

(b) Should be credited to separate account and shown in the balance sheet.

(c) Should be shown on the assets side

(d) None of these

Answer:

(c) Should be shown on the assets side

![]()

Question 3.

Subscription received by a school for organising annual function is treated as

(a) Capital Receipt

(b) Revenue Receipt

(c) Assets

(d) Earned Income

Answer:

(a) Capital Receipt

Question 4.

Out of the following items, which one is shown in the Receipts and Payments Account?

(a) Outstanding salary

(b) Depreciation

(c) Life Membership Fees

(d) Accrued subscription

Answer:

(d) Accrued subscription

Question 5.

The account is a summary of

(a) Income & Expenditure A/c

(b) Cash Book

(c) Balance sheet

(d) None of these

Answer:

(b) Cash Book

Question 6.

Capital fund is calculated-

(a) Income – Expenditure

(b) Assets – Liability

(c) Capital + Liability

(d) None of these

Answer:

(b) Assets – Liability

![]()

Question 7.

Subscription received in advance during the current year is

(a) An Income

(b) An Asset

(c) A Liability

(d) None of these

Answer:

(c) A Liability

Question 8.

Most transactions in non-trading concerns are-

(a) Cash

(b) Credit

(c) Cash and credit both

(d) None of these

Answer:

(a) Cash

Question 9.

If at the time of admission of a new partner, some profit & loss account balance appears in the books, it will be transferred to

(a) Profit and Loss Appropriation A/c

(b) All partners capital A/c

(c) Old partners capital A/c

(d) Revaluation A/c

Answer:

(b) All partners capital A/c

Question 10.

Assets and Liabilities are shown at their re-valued values in

(a) New balance sheet

(b) Revaluation A/c

(c) All partners capital A/c

(d) Realisation A/c

Answer:

(b) Revaluation A/c

![]()

Question 11.

If the Incoming partner brings the amount of goodwill in cash and also a balance exists in goodwill A/c, then this goodwill A/c is written off among the old partners in

(a) In new profit sharing ratio

(b) In old profit sharing ratio

(c) In sacrifice ratio

(d) In gaining ratio

Answer:

(b) In old profit sharing ratio

Question 12.

The amount of goodwill is paid by the new partner

(a) For payment of capital

(b) For sharing the profit

(c) For purchase of assets

(d) None of these

Answer:

(a) For payment of capital

Question 13.

Gaining Ratio is

(a) New Ratio – Sacrifice Ratio

(b) Old Ratio – Sacrifice Ratio

(c) New Ratio – Old Ratio

(d) Old Ratio – New Ratio

Answer:

(c) New Ratio – Old Ratio

Question 14.

On reconstitution of the firm, an increase in the value of assets will result in

(a) Gain to existing partners

(b) The loss to existing partners

(c) Neither gain nor loss to existing partners

(d) None of these

Answer:

(a) Gain to existing partners

![]()

Question 15.

Goodwill is a ______ asset

(a) Worthless

(b) Tangible

(c) Valueless

(d) Valuable

Answer:

(d) Valuable

Question 16.

Which accounts are opened when the capitals are fixed?

(a) Only capital accounts

(b) Only current accounts

(c) Liability account

(d) Capital and current A/c

Answer:

(d) Capital and current A/c

Question 17.

In the absence of a partnership deed, partners are not entitled to receive

(a) Salaries

(b) Commission

(c) Interest on capital

(d) All of these

Answer:

(c) Interest on capital

Question 18.

The relation of partners with the firm is that of-

(a) An owner

(b) An agent

(c) An owner and an agent

(d) Manager

Answer:

(a) An owner

Question 19.

Number of partners in an ordinary partnership firm maybe

(a) Maximum two

(b) Maximum ten

(c) Maximum twenty

(d) Maximum fifty

Answer:

(c) Maximum twenty

![]()

Question 20.

A preparing partnership deed is

(a) Compulsory

(b) Partly compulsory

(c) Voluntary

(d) None of these

Answer:

(a) Compulsory

Question 21.

Liability of partner is

(a) Limited

(b) Unlimited

(c) Determined by partnership Act

(d) None of these

Answer:

(b) Unlimited

Question 22.

The surrender value of an insurance policy means that value

(a) Which is received on the death of a partner.

(b) Which is received when a policy matures.

(c) Which can be received before the due date of the policy.

(d) None of the above

Answer:

(c) Which can be received before the due date of the policy.

Question 23.

On the retirement of a partner, goodwill will be credited to the capital account of

(a) Retiring partner

(b) Remaining partners

(c) All partners

(d) None of the above

Answer:

(b) Remaining partners

Question 24.

Partnership act provides that interest on the amount of capital balance left by the retiring partner be paid at

(a) 5%

(b) 6%

(c) Bank rate

(d) 8%

Answer:

(b) 6%

![]()

Question 25.

Excess of credit side over the debit side in Revaluation Account is

(a) Profit

(b) Loss

(c) Receipt

(d) Expense

Answer:

(a) Profit

Question 26.

Subject to the permission allowed, the maximum allowable discount on equity shares is

(a) 5%

(b) 10%

(c) 12%

(d) 20%

Answer:

(b) 10%

Question 27.

Amount of calls in Arrear is

(a) Added to capital

(b) Deducted from share capital

(c) Shown on the asset side

(d) Shown on the equity and liability side

Answer:

(b) Deducted from share capital

Question 28.

Forfeiture of shares results in the reduction of

(a) Paid-up capital

(b) Authorised capital

(c) Reserve capital

(d) Fixed assets

Answer:

(a) Paid-up capital

Question 29.

Discount allowed on the reissue of forfeited shares is debited to

(a) Share capital A/c

(b) Share forfeited A/c

(c) Profit & Loss A/c

(d) General reserve A/c

Answer:

(d) General reserve A/c

![]()

Question 30.

Company premium on issue of debenture is a

(a) Capital Gain

(b) Profit

(c) Revenue Receipt

(d) Asset

Answer:

(c) Revenue Receipt

Question 31.

Discount in the issue of Debentures is in the nature of

(a) Revenue Loss

(b) Capital Loss

(c) Deferred Revenue expenditure

(d) None of these

Answer:

(b) Capital Loss

Question 32.

On Liquidation of a company, the principal amount of debentures is returned

(a) First of all

(b) Last of all

(c) Before equity capital

(d) None of these

Answer:

(c) Before equity capital

Question 33.

Debenture holder receives

(a) Dividend

(b) Interest

(c) Both dividend and interest

(d) Bonus

Answer:

(b) Interest

Question 34.

According to SEBI guidelines, what percentage of the amount of debentures must be transferred to Debenture Redemption Reserve, before the commencement of redemption of debentures, in case of convertible debentures?

(a) 25%

(b) 50%

(c) 100%

(d) Zero

Answer:

(b) 50%

![]()

Question 35.

Profit on the redemption of debentures is transformed to which account?

(a) Capital Reserve Account

(b) Sinking Fund Account

(c) General Reserve Account

(d) Profit & Loss A/c

Answer:

(a) Capital Reserve Account

Question 36.

Proft on cancellation of own debenture is

(a) Revenue Profit

(b) Capital Profit

(c) Operating Profit

(d) Trading Profit

Answer:

(b) Capital Profit

Question 37.

Which of the following is correct profit or loss in case of the amount received from the sale of assets is Rs. 50,000, total assets is Rs. 60,000, total liabilities Rs. 20,000 and realisation exp. Rs.,2000?

(a) Rs. 8000 loss

(b) Rs. 12,000 loss

(c) Rs. 32,000 profit

(d) None of these

Answer:

(b) Rs. 12,000 loss

Question 38.

Sundry creditors amounted to Rs. 8000. These were paid at a discount of 5% Realisation A/c will be debited by

(a) Rs. 8000

(b) Rs. 7600

(c) Rs. 400

(d) Rs. 8400

Answer:

(c) Rs. 400

![]()

Question 39.

On dissolution of a firm, credit balance of partner’s capital account is paid to

(a) Partners

(b) Firm

(c) Wife

(d) None of these

Answer:

(a) Partners

Question 40.

On dissolution of the firm, partner’s capital A/c is closed through

(a) Realisation A/c

(b) Drawings A/c

(c) Bank A/c

(d) Loan A/c

Answer:

(c) Bank A/c

Question 41.

Which of the following is not a source of cash?

(a) purchase of fixed assets

(b) fund from operations

(c) issue of debentures

(d) sale of fixed assets

Answer:

(a) purchase of fixed assets

Question 42.

The ideal current ratio is

(a) 2 : 1

(b) 1 : 2

(c) 3 : 2

(d) 3 : 4

Answer:

(a) 2 : 1

![]()

Question 43.

The ideal debt equity ratio is

(a) 1 : 1

(b) 1 : 2

(c) 2 : 1

(d) 3 : 4

Answer:

(a) 1 : 1

Question 44.

Interpretation of financial statement includes

(a) criticism and analysis

(b) comparison and trend study

(c) drawing conclusion

(d) all of these

Answer:

(d) all of these

Question 45.

Dividends for the shareholders are

(a) payable tax amount

(b) tax-free amount

(c) interest

(d) none of these

Answer:

(d) none of these

Question 46.

Debenture holder receives

(a) dividend

(b) profit

(c) interest

(d) none of these

Answer:

(c) interest

![]()

Question 47.

Profit of cancellation of ‘Own debenture’ is transferred to

(a) profit & loss appropriation A/c

(b) debenture redemption A/c

(c) capital reserve A/c

(d) none of these

Answer:

(c) capital reserve A/c

Question 48.

The debenture is the part of

(a) share capital

(b) loan

(c) owned capital

(d) creditor

Answer:

(b) loan

Question 49.

Debenture carries interest at

(a) 12% p.a.

(b) 20% p.a.

(c) fixed rate

(d) 6% p.a.

Answer:

(c) fixed-rate

![]()

Question 50.

A company issues its shares at a premium under which Section of Indian Companies Act,1956?

(a) 78

(b) 79

(c) 80

(d) 81

Answer:

(c) fixed-rate

Non-Objective Type Questions

Short Answer Type Questions

Question No. 1 to 25 are Short answer type questions. Answer any 15 out of them. Each question carries 2 marks. (15 × 3 = 30)

Question 1.

State any three purposes for which share premium can be utilised?

Answer:

Following are the three purposes for which share premium can be utilised

- Issuing fully paid bonus shares to the members

- Writing off the preliminary expenses of Company

- In purchasing its own shares Buyback.

Question 2.

From the following information, calculate the stock turnover ratio.

Sales: Rs. 4,00,000

Average stock: Rs. 55,000

Gross Loss Ratio: 10%

Answer:

Sales = 4,00,000

Gross Loss Ratio = 10%

Average Stock = 55,000

Stock Turnover Ratio = Net sales/Avg. stock = 400000/55000 = 7.28 times

Question 3.

Prakash Industries issued Rs. 4,00,000, 9% debentures of Rs. 100 each on April 01, 2012, at a premium Of 6% redeemable at a premium of 10% on 31st March 2016. The debentures were redeemed on the due date. Pass only journal entries for the redemption of the debenture.

Answer:

In the Books of Prakash Industries.

Question 4.

Define the term DDL in RDBMS.

Answer:

A DDL is a language used to define data structure and modify data. For example, DDL commands can be used to add, remove or modify tables within a database. A data definition language has a pre-defined syntax for describing data.

![]()

Question 5.

Explain the primary key & candidate key.

Answer:

Primary key: A primary key is a column or a combination of columns that uniquely identify a record.

Candidate key: A candidate key can be any column or a combination of columns that can quality as a unique key in the database. There can be multiple candidate keys in one table. Each candidate key can quality as a primary key.

Question 6.

Explain Table, Record & Attributes in RDBMS.

Answer:

- Table: A table is a collection of data elements organised in terms of rows and columns.

- Records: Record in a table represents a set of related data.

- Attributes: The term “Attribute” is also used to represent a column. For example, in the Employee table, Name is a column that represents the names of the employee.

Question 7.

What is the chart in MS-Excel? Explain its importance.

Answer:

A chart is a powerful tool that allows you to visually display data in a variety of different chart formats such as Bar, Column, Pie, Line, Area, Doughnut. Scatter, Surface or Radar charts with Excel, it is easy to create a chart.

Following are the importance of chart:

- Visualization: Excel charts allow spreadsheet administrators to create visualizations of data sets.

- Automation: The Excel application automates the process of generating charts from existing data sets.

- Customisation: The chart functions in excel users to strike a balance between automation and customization.

- Integration: If a business or other organisation is using spreadsheet data managed within excel, using the chart function within excel aids integration of the data.

![]()

Question 8.

Mention any four provisions of the Partnership Act, in the absence of partnership deed.

Answer:

Following are the four provisions of the partnership Act, in the absence of partnership deed:

- Salary and commission

- Sharing of profits

- Interest on Capital

- Interest on Drawing

Question 9.

X and Y are partners. X’s capital is Rs. 10,000 and Y’s capital is Rs. 6,000. Interest is payable @ 6% p.a. on capital. Y is entitled to a salary of Rs. 200 per month. Profit for the current year is Rs. 8,000 before interest and salary to Y. Divide the profit between X and Y.

Answer:

Profit and Loss Appropriation Account.

Question 10.

What options are available to a company for allotment of debentures in case of over-subscription?

Answer:

In case of oversubscription following options available to a company:

- The excess application money on over applied debentures is refunded to the applicants

- Excess applications may be retained for adjustments towards allotment and call money. In such a case, applicants get pro-rata allotment

- Some applications may be rejected outright and applications money on such applications is returned.

Question 11.

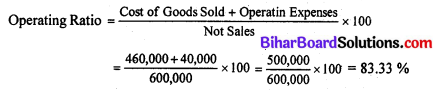

Calculate the operating ratio from the following data:

Sale: Rs. 6,40,000

Sales Return: Rs. 40,000

Cost of goods sold: Rs. 4,60,000

Operating expense: Rs. 40,000

Answer:

Calculation of operating Ratio:

where, Net Sales = Sales – Return = 640,000 – 40,000 = 600,000

Question 12.

A company took a loan of Rs. 2,00,000 from a Bank and placed with the Bank debentures for Rs. 2,50,000 as collateral securities. Show how they will appear in the company’s Balance Sheet.

Answer:

Balance Sheet

Question 13.

The Current Assets of a company are Rs. 15,00,000. Its Current ratio is 3 : 1 and Liquid ratio is 1.25 : 1. Calculate the amount of Current Liabilities, Liquid Assets and Inventory.

Answer:

Quick (liquid) Assets = (500,000 × 1.25) = 625,000

Inventory = Current Assets – QuickAssets = 1500,000 – 625,000 = 875,000

Question 14.

Explain absolute cell references in Excel.

Answer:

An absolute reference is designed in a formula by the addition of a dollar sign (&). It can precede the column reference, the row reference, or both.

Question 15.

Define RDBMS.

Answer:

A rational database management system (RDBMS) is a program that lets you create an update, and administer a relational database.

Question 16.

Explain the functions of SQL command in the following:

Alter & Update.

Answer:

The SQL ‘ALTER’ table command is used to add, delete or modify columns in an existing table.

The SQL ‘UPDATE’ command can update records for single table only.

![]()

Question 17.

Define types of SQL (DML & DCL).

Answer:

DML: Data manipulation language (DML) is used to retrieve, store, modify, delete, insert and update data in the database.

DCLA: data control language (DCL) is a syntax similar to a computer programming language used to control access to data stored in a database.

Question 18.

Explain Database design.

Answer:

Database design is the process of producing a detailed data model of a database. This data model contains all the needed logical and physical design choices and physical storage parameters needed to generate a design in a data definition language which can then be used to create a database. A fully attributed data model contains detailed attributes for each entity. The term data Dase design can be used to describe many different parts of the design of an overall database system.

Question 19.

Explain Schema & Subschema.

Answer:

Schema: 4 scheme is the design or layout of a database management system. It will often have a list of units or entities that feature in the database and describe the relationships between them. A schema often remains unchanged despite the volatile nature of the database.

Sub-schema: A sub-schema is. the best described as the way that the data in a DBMS appears when viewed by an application or a user.

Question 20.

Explain the financial function NPV ( ) in Excel with example.

Answer:

In finance Net present value (NDU) is defined as the sum of the present values of incoming and outgoing cash flows over a period of time.

![]()

Question 21.

Describe the pivot table in Excel, under ‘what-if analysis tool.

Answer:

By using ‘what-if analysis tools in Excel we can use several different sets of value in one or more formulas to explore all the various results.

Question 22.

Describe the processes of sorting in Excel.

Answer:

Excel provides a tool for sorting the given data according to multiple fields, you can sort your data on up to 64 different fields. The field may be Name, address, number, grades or any other field.

Question 23.

Write appropriate SQL commands to create an Employ table with required columns.

Answer:

The SQL create table statement is used to create a table to store data. Integrity constraints like primary key, unique key, a foreign key can be defined for columns while creating the employee table. The integrity constraints can be defined at the column level or table level.

Table Name i.e. column-1, column-2

Data type i.e. char, data, No, etc.

Question 24.

State four features of Income and Expenditure Account.

Answer:

Following are the Four features of Income and Expenditure A/c:

- It is a Nominal account.

- It is prepared from the Receipts and payments Account and other relevant information.

- Items are capital nature are not shown in this account.

- It shows the income and expenditure of the current year only on an accrual basis.

![]()

Question 25.

Distinguish between Fixed capital and fluctuating capital.

Answer:

Following are the differences between Fixed and Fluctuating capital A/c.

| Basis | Fixed Capital | Fluctuating Capital |

| 1. No of Accounts. | There are two accounts for each partner. Current A/c and capital A/c | There is only one account for each partner namely capital A/c |

| 2. Balance in capital A/c | The Balance in capital A/c remains the same year after year except under special circumstances. | The balance in capital A/c keeps on changing very frequently from year to year. |

| 3. Adjustments | Adjustments relating to drawings, interest on drawing, interest on capital etc. are made in current Account. | Adjustments relating to drawings, interest on capital etc. are made in capital Account. |

| 4. Nature of balance in Account. | Capital Account always shows a credit balance. Balance of current A/c Maybe either credit or debit. | Capital Account may have a debit balance or credit balance. Balance of current A/c does not arise in this case. |

Long Answer Type Questions

Question No. 26 to 33 are long answer type questions. Answer any 4 of them. Each question carries 5 marks. (4 × 5 = 20)

Question 26.

How would you calculate the amount payable to the retiring partner?

Answer:

Considering the following point, we can calculate the amount payable to the retiring partner.

(I) Entire amount co be paid in cash.

(i) If fund available:

Journal Entry:

Retiring partner’s capital A/c -Dr.

To Cash A/c

(ii) If the loan is taken from the bank:

(a) Bank or cash A/c -Dr.

To Bank loan A/c

(b) Retiring partner’s capital A/c -Dr.

To Bank or Cash A/c

(II) By transferring capital Balance into Retiring partner’s loan Account:

Journal Entry:

Retiring Partner’s Capital A/c -Dr.

To Retiring Partner’s Loan A/c

(III) Payment partly in cash and partly by transferring to loan A/c.

Journal Entry:

Retiring Partner’s Capital A/c -Dr.

To Cash A/c

To Retiring Partner’s Loan A/c

(IV) Payment of Retiring partner’s loan in Instalments.

Journal Entry:

(a) Interest A/c -Dr.

To Retiring Partner’s Loan A/c

(b) Retiring Partner’s Loan A/c -Dr.

To Cash or Bank A/c

(c) Profit & Loss A/c -Dr.

To Interest A/c

![]()

Question 27.

A, B arid C were partners in firm sharing profits in the ratio of 4 : 3 : 3. On 1.4.2013 they decided to dissolve the firm. On that date, A’s is capital was Rs. 1,25,000, B’s is capital was Rs. 45,000 and C’s capital was Rs. 15,000 (Dr.). The creditors amounted to Rs. 23,150 and cash in hand were Rs. 4,520. The assets realised Rs. 1,44,910 and the expenses of dissolution were Rs. 1,860. Prepare Realisation Account.

Answer:

The balance sheet on the date of dissolution is not given in the question. Hence Balance sheet on the date i.e. 1.09.2013 shall be prepared to ascertain the value of assets.

Question 28.

On 1st April 2013, Golu Ltd. was the holder of 500 shares of Rs. 10 each. He has paid Rs. 4 per share. At a meeting of the directors held on that date his shares were forfeited for non-payment of the first & final calls of Rs. 2 and Rs. 4 per share respectively. On 1st May 2013, these shares were re-issued fully paid to Maganlal for Rs. 4,500. Give Journal entries in the books of the company.

Answer:

Question 29.

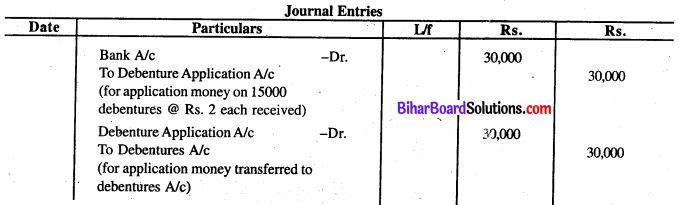

Satyam Ltd. issued 15,000 debentures of Rs. 10 each payable as follows: Rs. 2 on the application, Rs. 3 on the allotment, Rs. 5 on first & final calls. All the debentures were applied for and allotted. All money due was received, pass necessary journal entries.

Answer:

Question 30.

Journalise the following transactions for issue of debentures

(a) A debenture issued at Rs. 95 and redeemed at Rs. 100

(b) A debenture issued at Rs. 95 and will be redeemed at Rs. 105.

(c) A debenture issued at Rs. 100 and will be redeemed at Rs. 105.

Answer:

Question 31.

Calculate cash flow from operating activities from the following balances:

Answer:

Question 32.

From the following Balance Sheets of Goodluck Ltd. prepare cash flow statement according to Revised Accounting Standard 3 by the indirect method:

Answer: