BSEB Bihar Board 12th Accountancy Important Questions Long Answer Type Part 3 are the best resource for students which helps in revision.

Bihar Board 12th Accountancy Important Questions Long Answer Type Part 3

प्रश्न 1.

निम्नलिखित सूचना से देनदार आवर्त अनुपात की गणना करें :

उत्तर:

Working Notes :

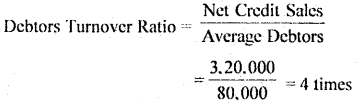

(1) Net Credit Sales = Total Sales – Cash Sales

4,00,000 – 80,000 (20% of 40,00,000) = 3,20,000

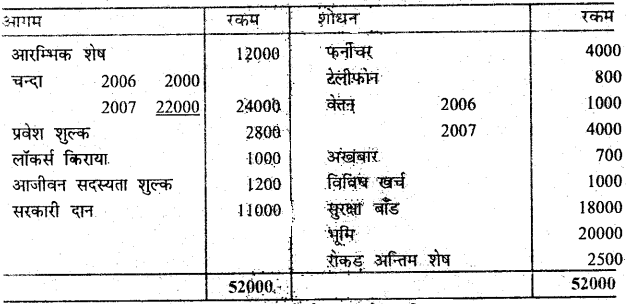

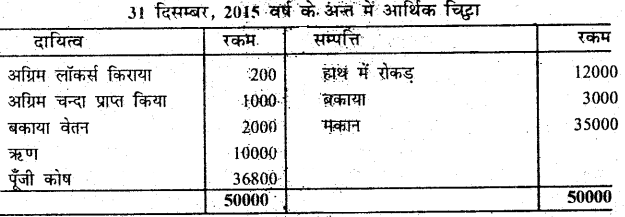

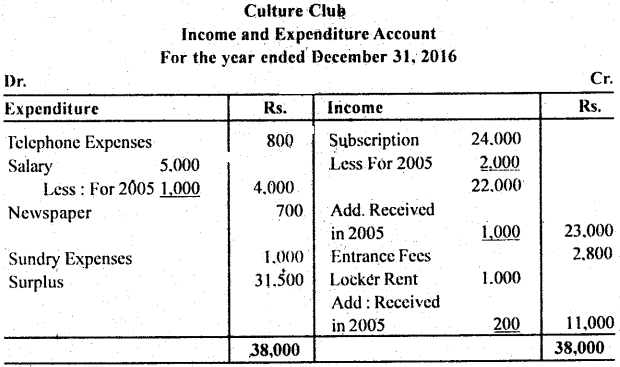

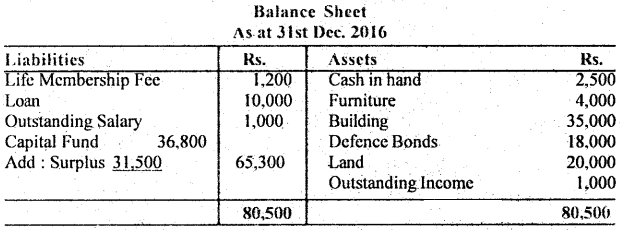

प्रश्न 2.

31 दिसम्बर, 2016 को समाप्त होने वाले वर्ष के लिए एक क्लब का आगम एवं शोधन सारांश निम्नांकित है। 31 दिसम्बर, 2016 को समाप्त होने वाले वर्ष के लिए एक क्लब का आय-व्यय बनाइए :

प्रवेश शुल्क एवं जीवन सदस्यता शुल्क का पूँजीकरण करना है। 2016 के चन्दे के 300 रु० अभी प्राप्त नहीं हुए। दिसम्बर 2016 का 170 रु० वेतन देना बाकी है। विनियोगों पर ब्याज 200 रु० मिलना बाकी है। छपाई व स्टेशनरी के 20 रु० अदत्त हैं।

उत्तर:

Insurance premium is usually paid for one year, hence it is assumed that Rs. 360 premium is for one year from 30th June, 2016 to 30th June, 2017. Therefore half of Rs. 360 (i.e., Rs. 180) is treated as prepaid.

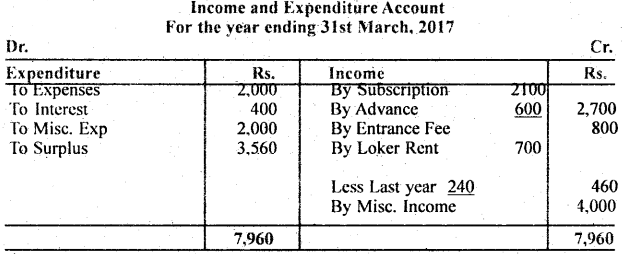

प्रश्न 3.

31 मार्च, 2017 को निम्न आगम एवं शोधन खाता और चिट्ठा के आधार पर आय-व्यय खाता तैयार करें।

उत्तर:

प्रश्न 4.

From the following Particulars taken the Cash Book of a Health Club, prepare a Receipts and Payments Account.

उत्तर:

प्रश्न 5.

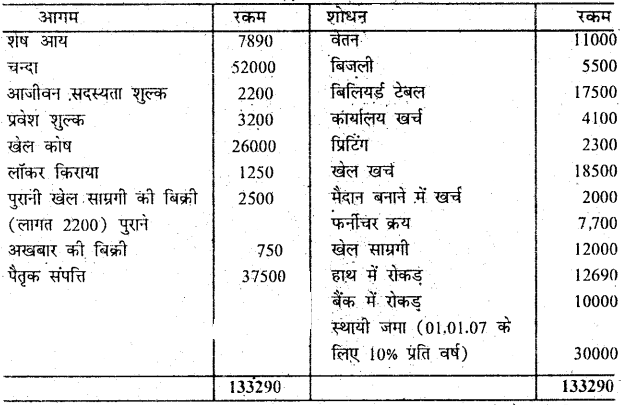

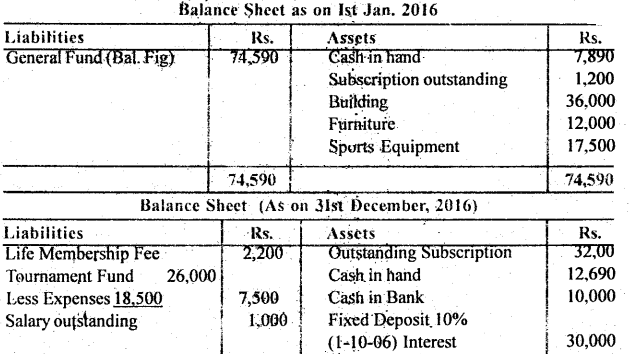

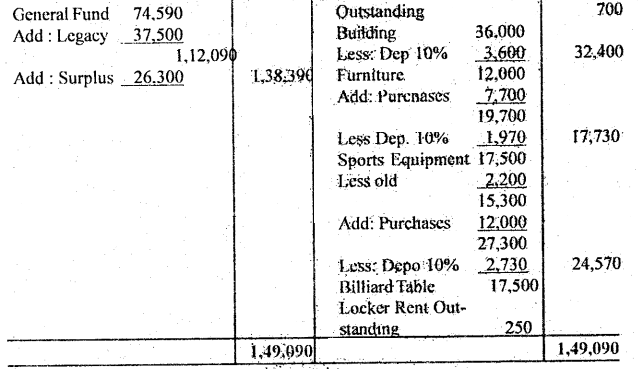

भारतीय स्पोर्ट्स क्लब के आगम और शोधन खातों की सूचना के आधार पर 31 दिसम्बर, 2016 का आय और व्यय खाता तथा आर्थिक चिट्ठा तैयार करें।

अलग सूचना-31 दिसम्बर, 2015. का बकाया चन्दा 1,200 रुपया और 31 दिसम्बर 2016 का 3200 बकाया लॉकर्स किराया 31 दिसम्बर, 2016 का 250 रुपया । बकाया वेतन 31 दिसम्बर का 1000 ।

1 जनवरी 2016 का क्लब के लिए मकान 36000 रुपया, फर्नीचर 12000 रुपया, खेल सामग्री 17500 रुपया । ह्रास इस मद में 10% (क्रय सहित)।

उत्तर:

प्रश्न 6.

आय और व्यय खाता तथा आर्थिक चिंटा 31 दिसम्बर, 2016 का बनायें।

उत्तर:

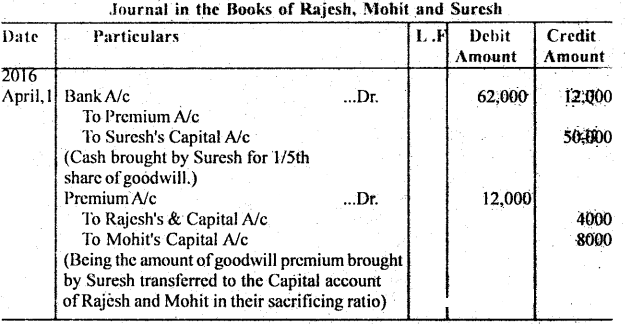

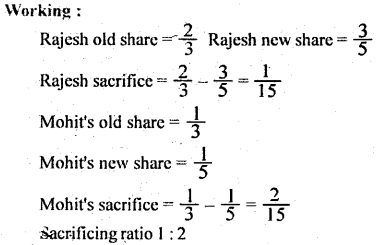

प्रश्न 7.

Rajesh and Mohit are partners there in a firmi sharing profits in the ratio 0f 2 : 1. Then admitted Suresh as a new partner for 1/5th share on April 1, 2016. The new profit sharing ratio of Rajesh, Mohit and Suresh will be 3 : 1 : 1 Suresh brought

Rs. 50,000 for his cupital and Rs. 12,000 as his share of premiun Record the necessury journal Entries for the treatment of goodwill premium in the book of the firm.

उत्तर:

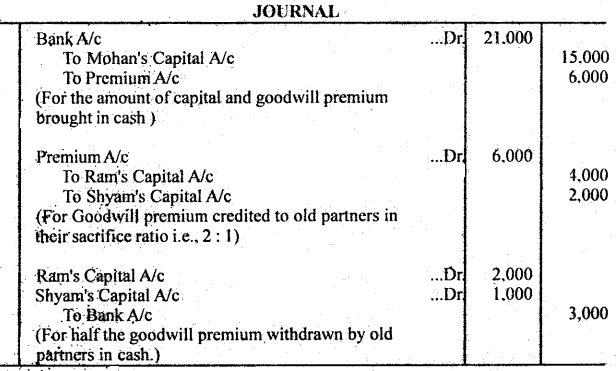

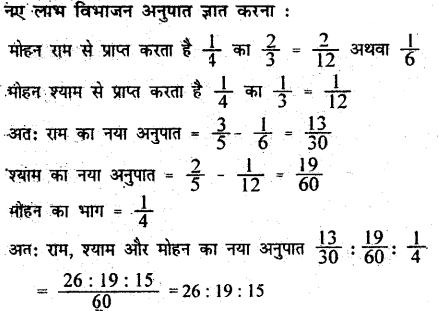

प्रश्न 8.

राम और श्याम साझेदार हैं। उनका लाभ-अनुपात 3 : 2 हैं। मोहन ने लाभों के 11 भागं के लिए साझेदारी में प्रवेश किया (जिसका 2/3 राम से और 2/3 श्याम से प्राप्त होता है)। मोहन 15,000 रु० पूँजी के लिए तथा 6,000 रु० ख्याति के लिए लाता है। ख्याति की राशि का आधा भाग पुराने साझेदारों द्वारा निकाल लिया जाता है।

आवश्यक जर्नल प्रविष्टियाँ कीजिए, तथा नया लाभ-विभाजन अनुपात ज्ञात कीजिए।

उत्तर:

प्रश्न 9.

A and B are partners sharing profits and losses in the ratio of 3 : 2. Their Balance Sheet on 31st December, 2016 stood as under:

On this date they admitted C for 25% share in profits on following term :

(i) C brings in Rs. 14,000 for his share of goodwill and further cash to make his capital proportionate to his share of profit.

(ii) Depreciate furniture by 10%

(iii) Half of investments were to be taken over by A and B in their profit sharing ratio and remaining valued at Rs. 26,000.

(iv) New ratio will be 3 : 3 : 2.

Prepare Revaluation Account, Capital Accounts and Balance sheet after C’s admission.

उत्तर:

Working Note:

1. C’s share of goodwill had been credited to A and B in their sacrificing ratio 9 : 1:

2. Capital brought in by C:

C’s share in profit = 25% or \(\frac { 1 }{ 4 }\)

For 3/4th share combined capital of A and B are C (Rs. 84,400 – Rs. 62,600) = Rs. 1,47,800

∴ Total Capital of firm = Rs. 1,47,000 × \(\frac { 3 }{ 4 }\) = Rs. 1,96,000

∴ C’s Share in total Capital = Rs. 1,96,000 × \(\frac { 1 }{ 4 }\) = Rs. 49,000

∴ Total Cash brought in by C: 14,000

C’s Capital Rs. 49,000 + Goodwill brought in Cash = 63,000

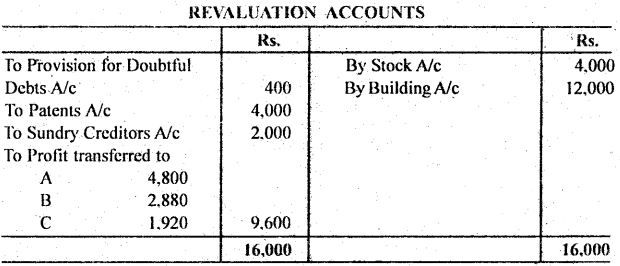

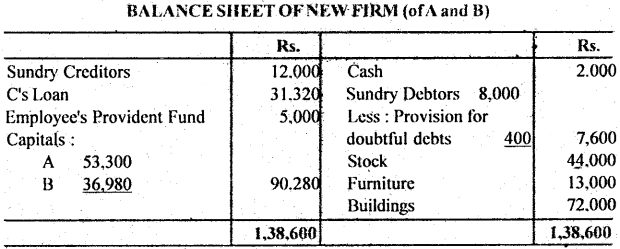

प्रश्न 10.

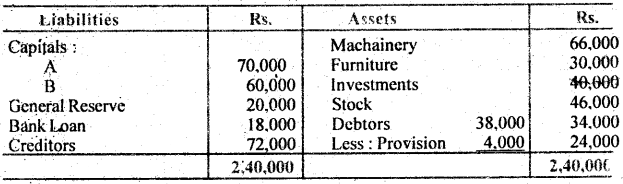

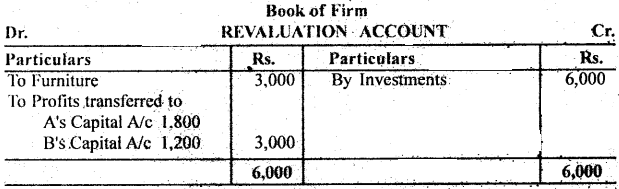

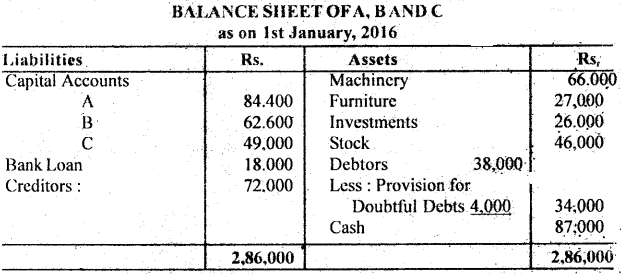

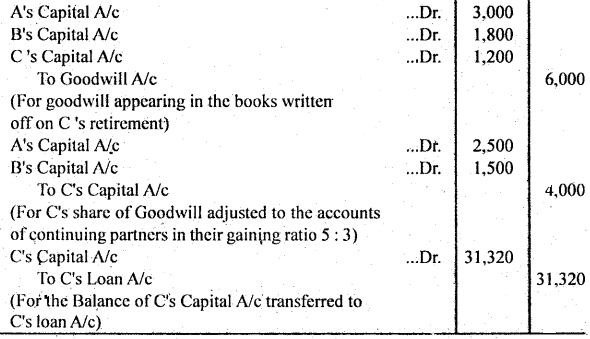

ए, बी और सी साझेदार हैं जो कि लाभ-हानि को 5 : 3 : 2 के अनुपात में बाँटते हैं। 1 जनवरी, 2016 को इनका चिट्ठा निम्नलिखित था।

सी उपर्युक्त तिथि को अवकाश ग्रहण करता है और साझेदारों में सहमति हुई कि :

1. ख्याति का मूल्यांकन गत चार वर्षों के औसत लाभ के आधार पर दो वर्षों का क्रय मूल्य के बराबर किया जाएगा । लाभ इस प्रकार थे : 2012 – 14,400 रु०, 2013 – 20,000 रु०, 2014 – 10,000 रु. (हानिः ), 2015 – 15,000 रु०।

2. संदिग्ध ऋणों के लिए आयोजन देनदारों पर 5% करना है।

3. रहतिया 10% से बढ़ाकर दिखाया जाएगा।

4. पेटेन्ट मूल्यरहित हैं।

5. भवन का मूल्य 20% से बढ़ाकर दिखाया जाएगा।

6. विविध लेनदारों को पुस्तक मूल्य से 2,000 रु० अधिक भुगतान करने पड़ेंगे।

जर्नल प्रविष्टियाँ बनाइए, पुनर्मूल्यांकन खाता, पूँजी खाते तथा नई फर्म का चिट्ठा तैयार

उत्तर:

Working Note:

1. ख्याति की गणना :

= 14,400 रु० + 20,000 रु० – 10,000 रु० (हानि) + 15,600 रु० + 40,000 रु० 40,000

औसत लाभ = \(\frac{40,000}{4}\)रु० = 10,000 रु०, ख्याति = 10,000 × 2 = 2000 रु०

2. किसी सूचना के अभाव में अवकाश ग्रहण करने वाले साझेदार का व्यय राशि को उस साझेदार के ऋण खाते में हस्तांतरित कर दिया जाता है।

3. ‘प्रॉविडेन्ट फन्ड .की राशि को कभी भी साझेदारों में पूँजी खातों में हस्तांतरित नहीं किया जाता है क्योंकि ये फर्म के ऊपर वास्तविक दायित्व हैं।

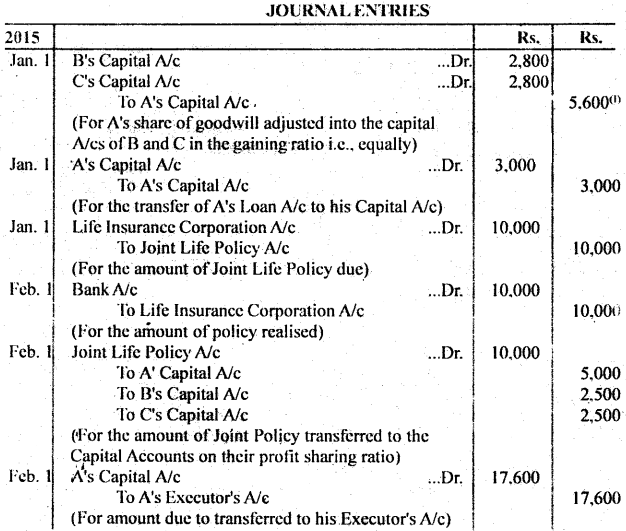

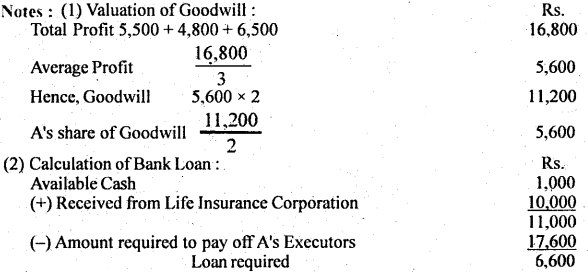

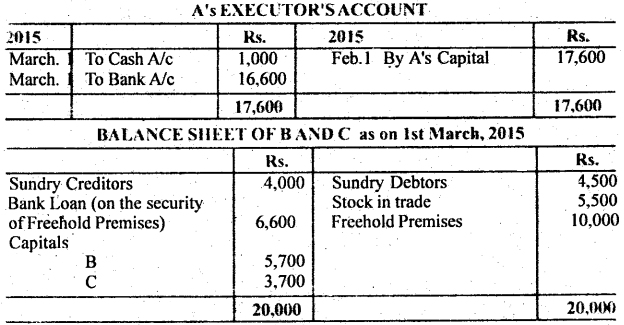

प्रश्न 11.

A, B and C were partners sharing profits in the proportion of one-half, one-fourth and one-fourth respectively. Their Balance Sheei on 31st December, 2004 was as follows:

A died on Ist January, 2015. The firm had affected an assurance of Rs. 10.000 on the joint lives of the three partners and the amount of the policy was realised on Ist Feb, 2015. According to the partnership agreement, the goodwill was to be calculated at two years purchase of averge profits of three completed years preceding the death or retirement of a partner. The deceased partner’s share of capital and goodwill etc. was paid out in cash on 1st March 2015 the available cash balance being supplemented by a loan from firm’s banker on the security of the frechold property. The net profits of the years 2012, 2013 and 2014 were Rs. 5,500, Rs. 4,800 and Rs. 6,500 respectively.

You are required to show the Journal entries, the ledger accounts to the partners and the Balance Sheet of B and C as it would stand after A’s share is paid out.

उत्तर:

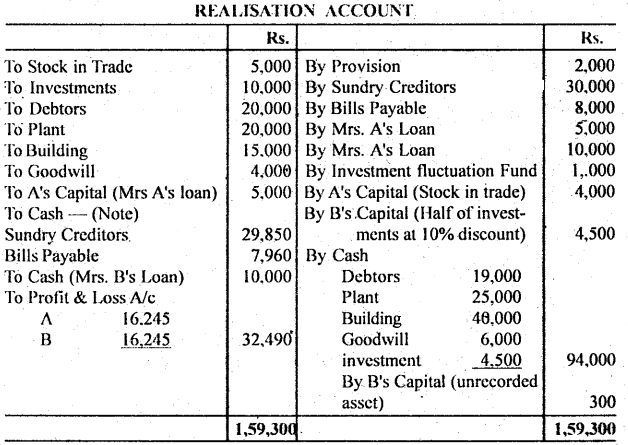

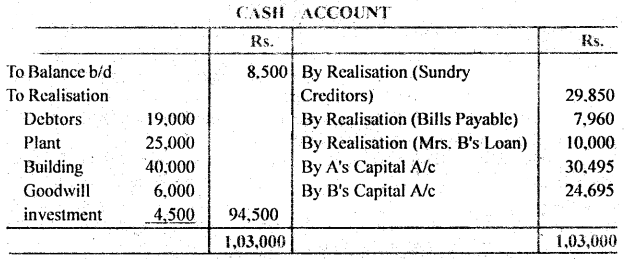

प्रश्न 12.

The following is the Balance Sheet of A and B as on 31st December 2016.

The firm was dissolved on 31st December 2016 on the following terms :

(a) A promised to pay Mrs. A’s loan and took away stock in trade at Rs. 4,000

(b) B took away half of the investments at 10% discount.

(c) Debtors realized Rs. 19,000

(d) Creditors and bills payable were due on an average basis on one month after 31st December, but they were paid immediated on 31st December 6% discount p.a.

(e) Plant realized Rs. 25,000 building Rs. 40,000 goodwill Rs. 6,000 and remaning invesments at Rs. 4,500.

(f) There was on old typewriter in the firm which had been written off completely from the books, it was estimated to realize Rs. 300, it was taken away by B at this estimated price.

You are required to prepare the (a) realisation A/c (b) partners’ capital A/c and (c) cash A/c to close books of the firm.

उत्तर:

Note (1):

Calculation of discount on Creaditors and Bills Payable :

Creditors – 30,000 × \(\frac{1}{12} \times \frac{6}{100}\) = Rs. 150

Bills payable – 8,000 × \(\frac{1}{12} \times \frac{6}{100}\) = Rs. 40

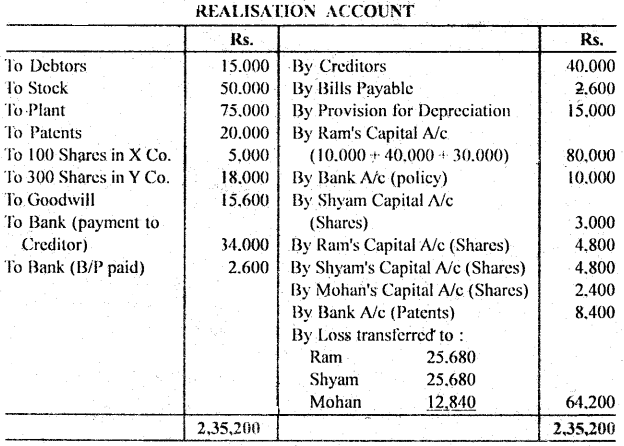

प्रश्न 13.

Ram, Shyam and Mohan shared profits in the ration of 2 : 2 : 1 Following is their Balance Sheet on the date of dissolution :

1. राम ने देनदारों को 10,000 रु० में, स्टॉक को 20% कम पर तय को 30,000. रु. में लिया ।

2. एक लेनदार ने कुछ पेटेन्ट, जिनका पुस्तक मूल्य 8,000 रु० था, 4,800 रु० निर्धारित मूल्य पर ले लिया। शेष लेनदारों को 1,200 रु० छूट पर भुगतान कर दिया गया ।

3. 20,000 रु० की एक संयुक्त जीवन बीमा पॉलिसी थी. (जो चिट्टे में नहीं दिखाई गई है) यह 10,000 रु० में समर्पण कर दी गई ।

4. एक्स कम्पनी के अंशों को श्याम 30 रु० प्रति अंश की दर से लेने को सहमत हो गया।

5. वाई कम्पनी के अंशों को मूल्यांकन 12,000 रु० पर किया गया । इन अंशों को सभी साझेदारों ने लाभ विभाजन अनुपात में बाँट लिया ।

6. शेष पेटेंट्स से पुस्तक मूल्य का 70% वसूल हुआ । आवश्यक खाते बनाइए ।

उत्तर:

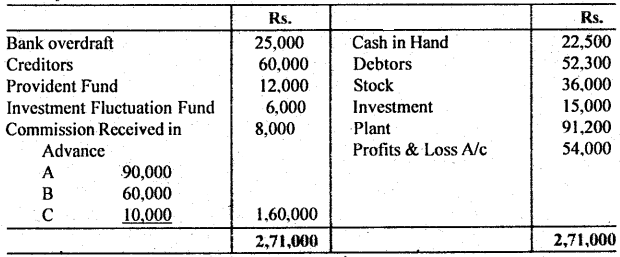

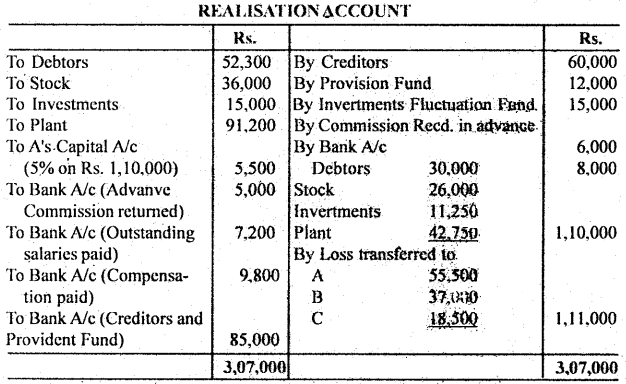

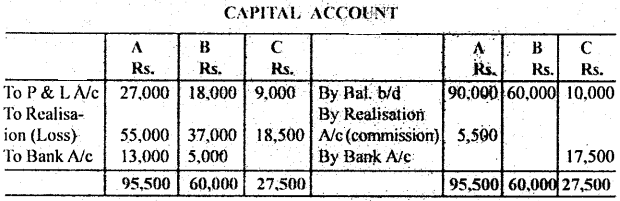

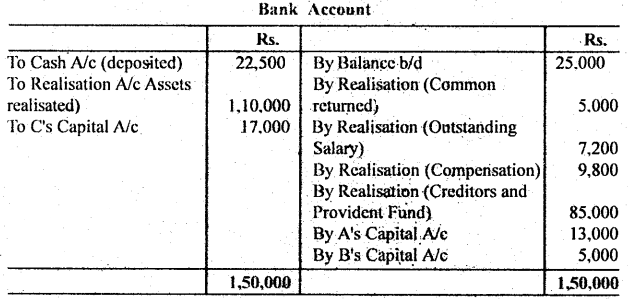

प्रश्न 14.

A, B and C shared profits in the ratio of 3 : 2 : 1. They dissolved the firm, and appointed A to realise the assets. A is to receive 5% commission on the sale of assets (except cush) and is to bear all expenses of realisation. The position of the firm was as follows:

Informations :

1. A realised the assets as follows :- Debtors Rs 30,000 Stock Rs.26,000; Investment at 75% value: Plant at Rs. 42,750. Expenses of realisation amounted to Rs. 4,100

2. Commission received in advance is retured to the customers after deducing Rs. 3,000 for work done.

3. Firm had to pay Rs.7,200 for outstanding salaries, not provided for carlied.

4. Compensation to employees paid by the firm amounted to Rs. 9,800. This liability was not provided for in the above balance sheet.

5. Rs. 25,000 had to be paid for provident Fund:

उत्तर:

नोट : 1. वसूली व्ययों की कोई प्रविष्टि नहीं की जाएगी। क्योंकि इन्हें ए स्वयं सहन करेगा

2. सम्पत्तियों के विक्रय पर ए को जो कमीशन मिलेगा, उसकी निम्न प्रविष्टि होगी :

Realisation A/c …Dr. 5,500

To A’s Capital A/c 5,500

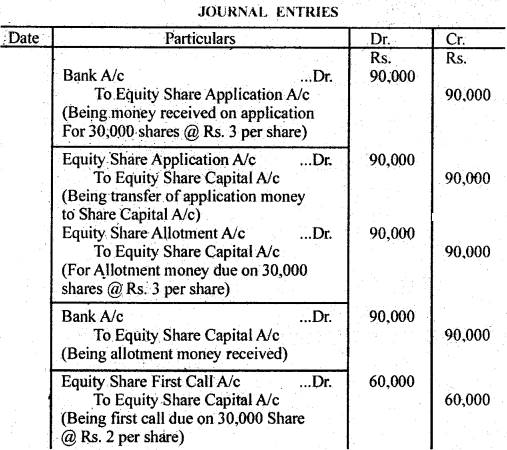

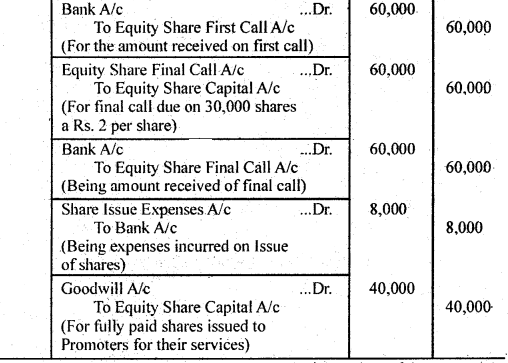

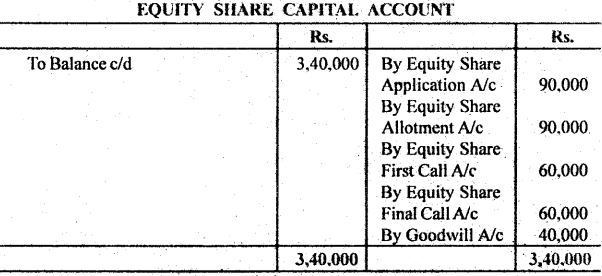

प्रश्न 15.

पवन लिमिटेड ने 10 रु० वाले 30.000 अंशों के लिए प्रार्थना पत्र आमन्त्रित किए। भुगतान निम्न प्रकार होना था- आवेदन पर 3 रु०, आवंटन पर रु०, प्रथम याचना पर 2रु० और अन्तिम याचना पर 2 रु०।

सभी अंशों के लिए प्रार्थना पत्र आए। यह मानते हुए कि आवंटन और याचनाओं पर देय सभी राशियाँ प्राप्त हो गई हैं, आप जर्नल प्रविष्टियाँ खाते तथा प्रारम्भिक स्थिति विवरण तैयार कीजिएं। अंशों के निर्गमन के व्यय 8,000 रु० हुए। प्रवर्तकों को उनकी सेवाओं के लिए 4,000 पूर्णदत्त अंशों का निर्गमन किया गया।

उत्तर:

टिप्पणी : 1. आवेदन राशि प्राप्त होने की प्रविष्टि को पहले बनाया गया है और इस अंश को पूँजी खाते (Share Capital A/c) में हस्तांतरित करके प्रविष्टि को इसके बाद बनाया गया है। इसका कारण यह है कि आवेदन के समय पहले राशि प्राप्त होती है।

2. आवेदन, प्रथम याचना और द्वितीय याचना के समय पहले अंश पूँजी खाते से हस्तांतरण की प्रविष्टि बनाई गई है तथा इसके पश्चात् ही राशि प्राप्त होने की प्रविष्टि बनाई जाती है। इसका कारण यह है कि इन राशियों के याचनाओं के समय ही हस्तांतरण को प्रविष्टि बने होते हैं जबकि राशि बाद में प्राप्त होती रहती है।

3. यदि अंशों का प्रकार (Type of Shares) स्पष्ट नहीं है. तो अंशों को हमेशा. समता अंश (Equity Shares) माना जाएगा।

प्रश्न 16.

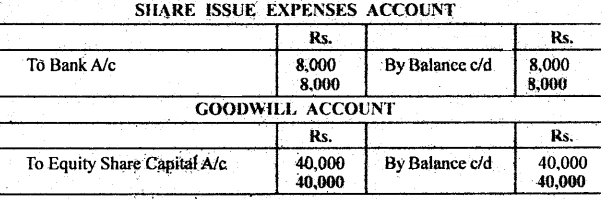

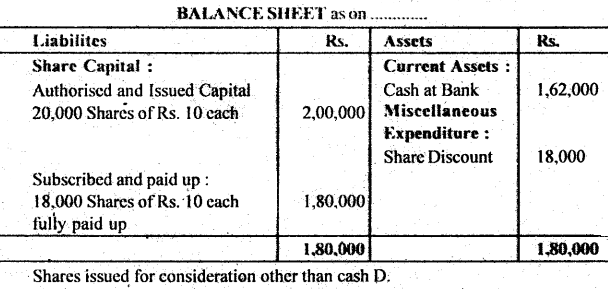

Shiva Ltd. issued 20,000 shares of Rs. 10 cach at a discount of 10%. Payments were to be made as on Application Rs. 3 on Allotnient Rs. 4 and of First and Final Call Rs. 2.

Applications were received for 18,000 shares and all were accepted All money was duly received.

Pass necessary entries in the Books of Company and also show the Balance Sheet of the Company.

उत्तर:

प्रश्न 17.

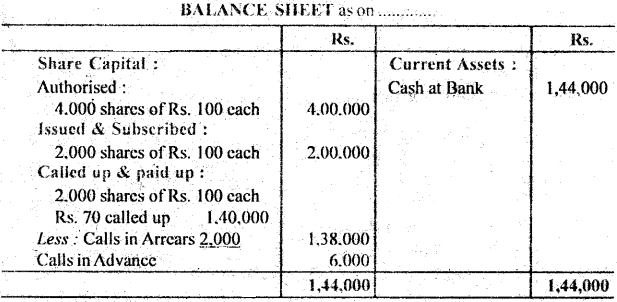

सनराइज लिमिटेड 4,00,000 रु० की पूँजी से समामेलित हुई। प्रत्येक अंश 100 रु० का है। इनमें से 2,000 अंश निर्गमित किए गए जिन पर आवेदन के साथ 25 रु प्रति अंश, आवंटन पर 25 रु०, प्रथम याचना पर 20 रु० तथा आवश्यकता पड़ने पर शेष राशि देय थी।

प्रार्थना-पत्र तथा आवंटन पर देय सभी राशियाँ यथासमय प्राप्त हुईं, परन्तु जब 20 रु० की प्रथम याचना मांगी गई थी तो एक अंशधारी जिसके पास 100 अंश थे, देय राशि नहीं दे पाया दूसरे अंशधारी ने जिसके पास 200 अंश थे, समस्त भुगतान कर दिया।

कम्पनी के जर्नल में इन लेन-देनों का लेखा कीजिए तथा कम्पनी का प्रारम्भिक स्थिति विवरण भी तैयार कीजिए।

उत्तर:

संकेत : प्रश्न में द्वितीय याचना नहीं मँगाई गई है, अतः प्रश्न केवल प्रथम याचना तक ही करना है।

प्रश्न 18.

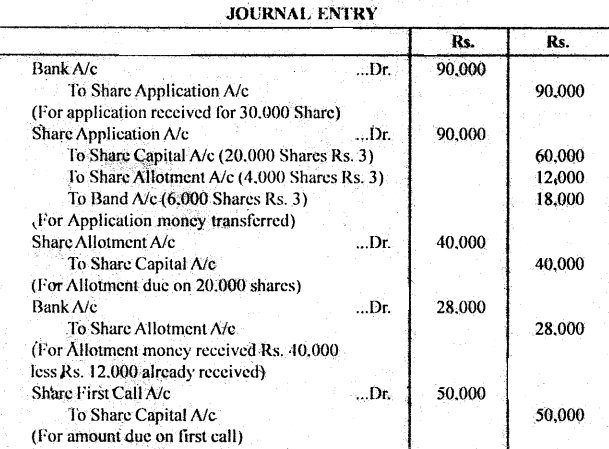

X Ltd invited application for 20,000 Shares of Rs. 10 each payable as follows: Rs. 3 on application. Rs. 2 on Allotment Rs. 2.50 on first Call and Rs. 2.50 on Second Call.

Public applied for 30,000 Shares and the allotment were made as under

To Applicants for 8,000 Share ………. full

To Applicants for 16,000 share …… 12,000 Share

To Applicants for 6,000 Share ………….. Nil

All money were duly received. Pass Journal Entry.

उत्तर:

प्रश्न 19.

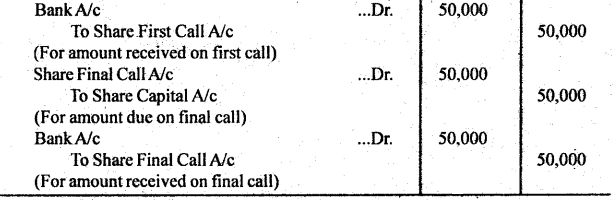

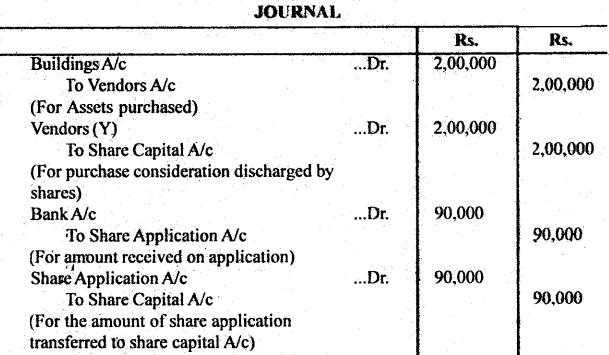

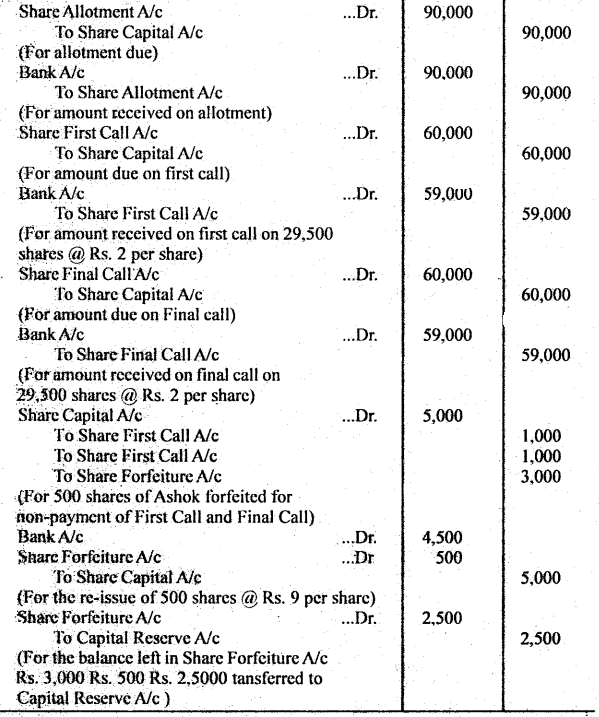

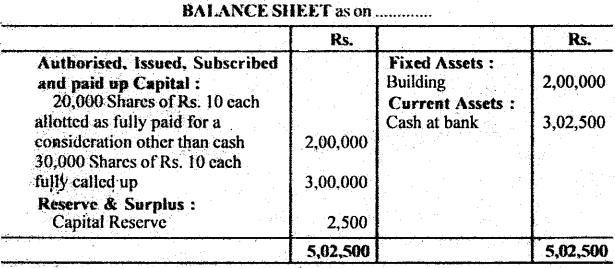

पवन लिमिटेड 5,00,000 रु० की अधिकृत पूँजी से समामेलित की गई जो कि 10 रु० प्रति अंश में विभाजित है। कम्पनी ने वाई से 2,00,000 रु० का एक भवन खरीदा जिसके बदले में वाई को कम्पनी के पूर्णदत्त अंश दे दिए गए। कम्पनी ने शेष 30,000 अंशों के लिए प्रार्थना-पत्र आमन्त्रित किए जो निम्न प्रकार देय थे-3रु प्रति अंश आवेदन पर, 3रु० प्रति अंश आवंटन पर, 2 रु० प्रति अंश प्रथम याचना पर और शेष 2 रु० अन्तिम याचना पर।

अंशोक, जिसको 500 अंश आवंटित किए गए थे, वह दोनों याचनाओं की राशि देने में असमर्थ रहा। उसके अंशों का हरण कर लिया गया और बाद में हरि को 9 रु० प्रति अंश पर, पूर्णदत्त में पुनः निर्गमन कर दिया। जर्नल में आवश्यक प्रविष्टियाँ बनाइए तथा कम्पनी का प्रारम्भिक स्थिति विवरण भी बनाइए।

उत्तर:

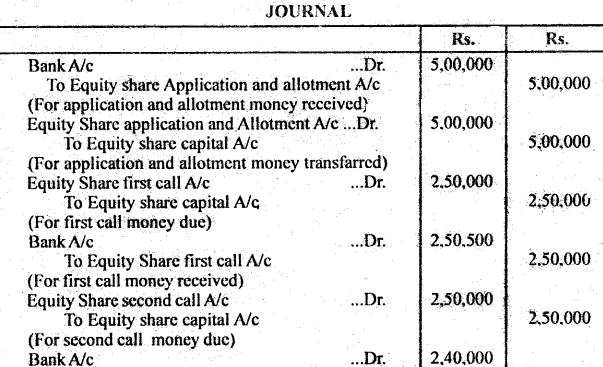

प्रश्न 20.

A Ltd. makes an issue of 10,000 equity shares of Rs. 100 each, payable as follows. On application and allotment – Rs. 50

On first call – Rs. 25

On second call – Rs. 25

Members holding 400 shares did not pay the second call and the shares are duly forfeited, 300 of which are re-issued as fully paid at Rs. 80 per share. Pass Journal entries in the books of the company.

उत्तर:

टिप्पणी : (1) पूँजी संचय (Capital Reserve) खाते में केवल उन्हीं अंशों का लाभ हस्तांतरित निजाता है, जिन्हें पुनः निर्गमित किया गया है । इस प्रश्न में केवल 300 अंशों का पुनः निर्गम ले । गया है । अत: 300 अंशों के लाभ को ही पूँजी संचय में हस्तांतरित किया जाएगा ज्ञात किया जाएगा :